Market downturns are an inevitable part of investing. Bear markets will come, and while you can’t avoid them, how you respond matters most. If your portfolio is aligned with your investment timeline and risk tolerance during stable periods, sudden market turbulence may not cause as much anxiety. In this context, author Liz Ann Sonders explains the importance of strategic planning and disciplined portfolio management function as a preemptive risk management tool, akin to hedging against volatility before market turbulence occurs, much like taking Dramamine to prevent motion sickness before a bumpy ride.

Sonders delves into the factors of the market, where a common reaction is a panic, manifesting itself in selling off investments as prices fall. This is a surefire way to flip the age-old wisdom of “buy low, sell high” on its head. Today, more than ever, economic data and market updates are readily available, and trading is easy and affordable. These factors can heighten our impulse to react quickly, though often to our detriment.

Greed, on the other hand, tempts investors to chase higher-risk assets in hopes of substantial returns. However, the potential for higher rewards comes with a darker side—greater risk. Portfolios that lean heavily on aggressive strategies often experience higher volatility and more significant drawdowns. Importantly, the best returns are usually achieved not through lucky bets, but by sticking to a long-term approach.

Another temptation investors face is trying to time the market—predicting the next big upswing or downturn and adjusting investments accordingly. Unfortunately, very few tools or strategies can reliably do this. Greed can often lead to panic down the line. Investors may think they know their risk tolerance, but the emotional reality of market downturns often reveals a gap between what they thought they could handle financially and what they can emotionally tolerate.

Sonders explains that many investors fall into the trap of making decisions based on past performance, believing it will predict future results. Experienced investors nearing retirement maintain aggressive strategies because they are used to the excitement of big gains, without fully considering how a major loss could affect their savings. On the other hand, some young investors are overly cautious, avoiding any significant losses despite having decades to recover and grow their portfolios.

Aggressive investors often learn the hard way that they aren’t as comfortable with short-term losses as they initially thought. Maintaining these strategies requires rebalancing, which sometimes means doubling down on asset classes that have underperformed while moving away from those that fared better during market downturns. Conservative investors, too, must understand that lower-risk portfolios may offer stability, but this often means sacrificing upside potential during bull markets. Many investors unrealistically want the best of both worlds—all the upside without any downside.

One of the most valuable practices in investing is periodic rebalancing. This involves adjusting your portfolio by adding to underperforming assets and trimming those that have outperformed, which can be challenging emotionally. However, maintaining the right asset mix over time is one of the most critical decisions investors can make. Sonders notes that rebalancing forces investors to stick to the principle of “buy low, sell high,” or in this case, “add low, trim high.”

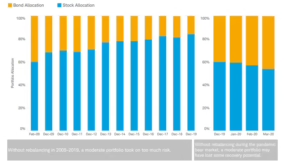

Without rebalancing, a portfolio can become unbalanced and take on too much risk. For example, an investor who didn’t rebalance 60% of equities and 40% bonds portfolio between 2009 and 2019 would have seen their equity exposure grow to nearly 85%, just before the COVID-19 bear market. When markets corrected, the lack of rebalancing reduced the portfolio’s potential for recovery.

The discipline of annual rebalancing helps keep portfolios on track. If investors neglect this practice, they risk overexposure to certain asset classes, especially during periods of significant market movement. Rebalancing not only manages risk but also ensures that portfolios remain aligned with long-term financial goals.

Asset allocation, diversification, and regular rebalancing are how you can make the most out of investing. One of Schwab’s key pieces of advice is the importance of having a long-term strategic asset allocation plan. While creating such a plan isn’t the hardest part, sticking to it—especially during volatile markets—often is.

By reflecting on previous missteps and incorporating those lessons into your investment strategy, you can mitigate the likelihood of repeating costly errors. Maintaining a disciplined approach, particularly in the face of market volatility, ensures that emotional decision-making—often driven by fear or greed—doesn’t derail your long-term financial goals.

The author elucidated the differences between panic and greed why depicting the various strategies an investor can use. A well-structured portfolio, aligned with your risk tolerance and investment horizon, serves as a critical tool in guiding the rebalancing process. Rebalancing is essential for managing risk and maintaining the optimal asset allocation, which helps capitalize on market opportunities while reducing exposure to unnecessary risks. Over time, these practices seek to improve your overall portfolio performance but also enhance your probability of pursuing consistent, sustainable investment success.

This research material has been prepared by LPL Financial

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual. To determine which investment(s) maybe appropriate for you, consult your financial advisor prior to investing. All performance referenced is historical and is no guarantee of future results. All indices are unmanaged and may not be invested into directly.

There is no guarantee that a diversified portfolio will enhance overall returns or outperform a non-diversified portfolio. Diversification does not protect against market risk.

Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

Rebalancing a portfolio may cause investors to incur tax liabilities and/or transaction costs and does not assure a profit or protect against a loss.

Asset allocation does not ensure a profit or protect against a loss.